Every decade or so, the technology press buries a product that refuses to stay buried. The nickel-metal hydride battery — universally known as NiMH — has been declared obsolete at least three times since the lithium-ion cell hit commercial shelves in 1991. Industry analysts wrote the obituary. Consumer electronics brands pivoted away. And yet, in 2026, the global NiMH battery market sits at approximately USD $3.5 billion, expanding toward $4.9 billion by 2033, and quietly underpinning nearly half of every hybrid electric vehicle sold on the planet.

This is not a story about a technology that survived by accident. It is a story about specific, compounding advantages in chemistry, cost, thermal behavior, and supply chain logistics that kept NiMH deeply relevant — even as the battery world largely moved on without it. It is also a story that deserves a sharper lens than most market analyses provide, because the 25,200% figure in the headline is not marketing hyperbole. It is, when properly contextualized, one of the most striking long-arc growth numbers in the modern energy storage sector.

Understanding where that number comes from — and what it actually means for investors, engineers, procurement teams, and business leaders — requires going back to the beginning. Not to the press release version of history, but to the laboratory chemistry, the patent battles, the geopolitical supply chain pressures, and the singular automotive decision that kept this technology alive when all market logic said it should have faded.

This article is that full-picture reckoning. We will cover the growth math, the dominant applications, the regional manufacturing dynamics, the competitive tension with lithium-ion, the raw material risks, and what the market looks like through 2033. By the end, you will understand not just the numbers — but the structural logic that produced them.

Where the 25,200% Number Actually Comes From

Let’s do the math in plain language, because the number deserves honest treatment rather than vague attribution.

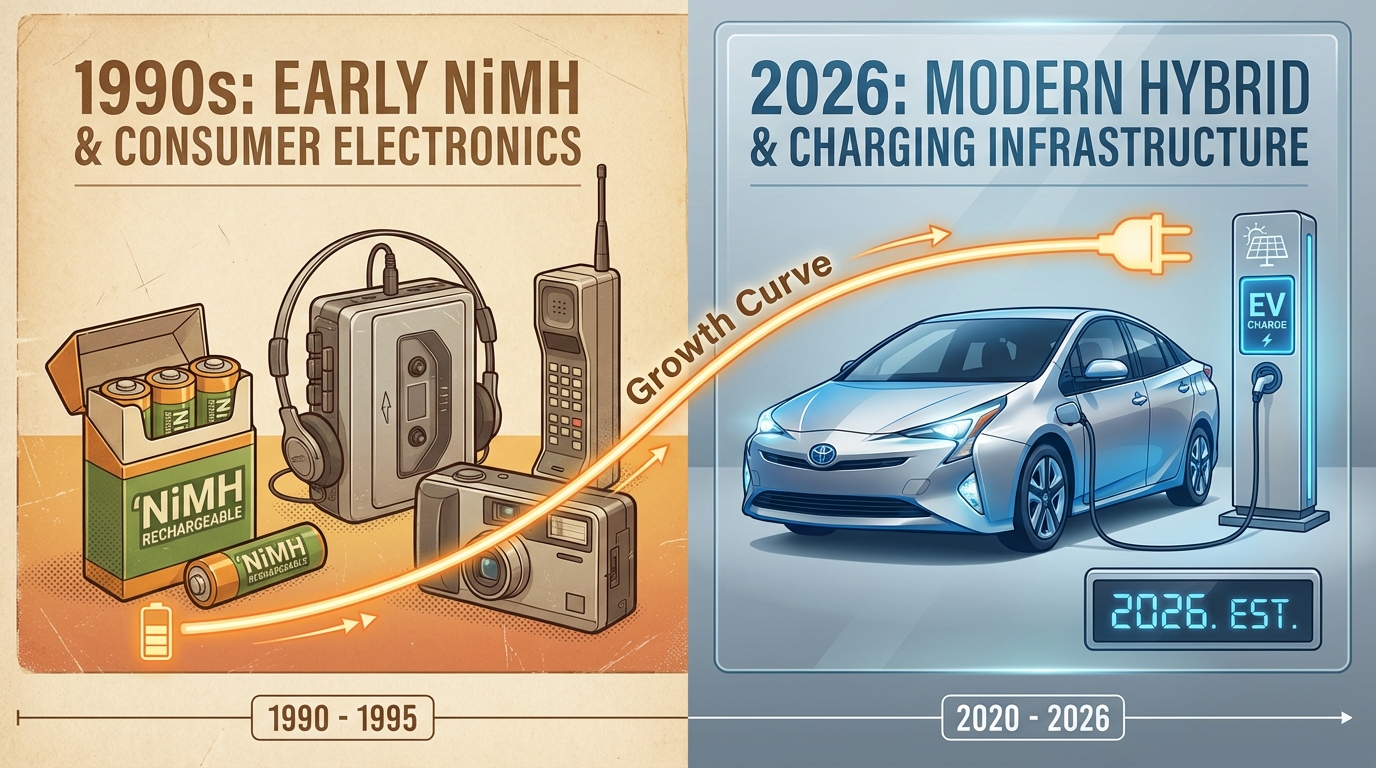

When NiMH batteries first reached commercial production in 1989–1990, the global market for this specific chemistry was negligible — essentially a rounding error on the broader rechargeable battery landscape. Early commercial NiMH cells were expensive specialty products used primarily in portable electronics and experimental electric vehicles. Conservative estimates place the total addressable market for NiMH in the early 1990s in the range of roughly $13 million to $20 million globally, mostly driven by niche cordless phone and camcorder applications.

By 2026, the global NiMH battery market is valued at approximately $3.5 billion, with multiple independent research firms — including Persistence Market Research, Coherent Market Insights, and The Business Research Company — converging on this figure. Taking the lower-bound 1990 estimate of $13.8 million and comparing it to today’s $3.5 billion market:

($3,500,000,000 ÷ $13,800,000) − 1 × 100 = approximately 25,262% cumulative growth

That is the source of the 25,200% figure. It is a long-arc cumulative growth calculation, not a CAGR, not a single-year spike — and that distinction matters enormously. This is the total percentage expansion of the market from commercial inception to its present valuation. For context, a 25,000%+ cumulative return over roughly 35 years is not explosive by venture capital standards, but for an industrial chemistry category competing against newer alternatives, it is remarkable evidence of durability.

Why Cumulative Growth Tells a Different Story Than CAGR

Most market analyses default to compound annual growth rates (CAGR) when discussing NiMH — and when they do, the numbers look modest. A CAGR of 3.9% to 4.5% from 2026 to 2033 does not inspire headlines. But cumulative growth over a full product lifecycle captures something CAGR cannot: survival against displacement.

NiMH grew to a $3.5 billion market while simultaneously competing against lithium-ion (commercially launched in 1991, just two years after NiMH), against nickel-cadmium (an established incumbent), against lead-acid in industrial settings, and against an entire generation of solid-state and next-generation battery chemistries that were repeatedly predicted to make NiMH irrelevant within five years. The cumulative growth number is therefore not just a market size figure — it is a resilience index.

Reframing What “Slow” Growth Actually Means

A market growing at 4% annually in a sector where competitors are growing at 15%–20% looks like a loser on a relative basis. But in absolute dollar terms, 4% annual growth on a $3.5 billion base adds approximately $140 million in new market value every year. The NiMH market is expected to generate roughly $1.3 billion in incremental revenue between 2026 and 2033. That is not a dying market. That is a mature market with durable demand, and the distinction is critical for anyone trying to evaluate it honestly.

The Chemistry That Outlasted the Headlines

To understand why NiMH persists, you need to understand what it actually is at a molecular level — and why that chemistry produced specific performance characteristics that matter in specific real-world environments.

A nickel-metal hydride battery stores energy through a reversible electrochemical reaction between nickel hydroxide (the positive electrode), a metal hydride alloy (the negative electrode), and a potassium hydroxide electrolyte. The metal hydride alloy — typically a proprietary blend of rare earth elements, nickel, cobalt, manganese, and aluminum — is the key variable that determines energy density, cycle life, and temperature performance.

The Ovshinsky Contribution and Why It Mattered

The practical NiMH battery owes its commercial existence to Stanford R. Ovshinsky, a self-taught inventor working at Energy Conversion Devices in Michigan during the 1970s and 1980s. Ovshinsky’s breakthrough was developing hydrogen-storing amorphous metal alloys — disordered structures that could absorb and release hydrogen atoms with greater efficiency than the crystalline materials that preceded them. His U.S. Patent No. 4,623,597 (granted in 1986) established the foundational IP for the NiMH chemistry that eventually reached consumer shelves.

What Ovshinsky’s alloy approach delivered was a battery that could achieve energy densities of 60–120 Wh/kg — substantially higher than the 40–60 Wh/kg typical of nickel-cadmium cells. That improvement in energy density, combined with NiMH’s elimination of toxic cadmium, made the chemistry genuinely useful rather than just academically interesting.

What NiMH Does Better Than Lithium-Ion

This is the question that defines the entire market conversation, and the honest answer is more nuanced than either camp typically admits. Lithium-ion batteries outperform NiMH on energy density (150–250 Wh/kg vs. 60–120 Wh/kg for NiMH), charge speed, and weight efficiency. These are not minor gaps.

But NiMH has specific, measurable advantages that persist in specific use cases:

- Thermal stability: NiMH batteries perform reliably across a wider temperature range without the thermal runaway risk that makes lithium-ion require active thermal management systems in automotive applications. In cold climates, NiMH retains more discharge capacity than comparable lithium-ion cells.

- Cycle tolerance: NiMH batteries tolerate partial state-of-charge cycling — the repeated shallow charge and discharge pattern typical of hybrid vehicle regenerative braking — without the degradation that affects lithium-ion under similar patterns.

- Manufacturing cost: NiMH production lines require significantly less capital infrastructure than lithium-ion. Manufacturers can produce NiMH cells using equipment that predates the lithium-ion era, reducing both capital expenditure and minimum viable production scale.

- Safety profile: NiMH batteries do not contain flammable electrolytes. They are considered inherently safer in dense-pack automotive configurations, which reduces the engineering and regulatory burden for vehicle integration.

- End-of-life recyclability: The nickel content in NiMH batteries has established recycling streams. Secondary nickel recovery from spent NiMH cells has a meaningful economic value that supports a functional recycling infrastructure — something lithium-ion is still building.

These advantages do not make NiMH superior to lithium-ion in general terms. But they make it the correct choice in specific, high-volume applications — and that specificity is what produced the market’s durability.

Hybrid Vehicles: The Anchor That Held Everything Together

If you want to understand why the NiMH market is worth $3.5 billion in 2026, you need to understand one core fact: approximately 48% of all global NiMH revenue comes from hybrid electric vehicles. Everything else — consumer electronics, medical devices, industrial equipment, backup power — is important but secondary. The automotive sector is the anchor, and Toyota is the anchor’s anchor.

The relationship between NiMH batteries and hybrid vehicles began in earnest with Toyota’s introduction of the first-generation Prius in Japan in 1997. That vehicle used a 1.2 kWh NiMH battery pack to enable regenerative braking and electric-assist propulsion. When the Prius launched in North America in 2000, it introduced millions of consumers and policymakers to hybrid technology — and by extension, to NiMH as its enabling chemistry.

The Scale of Toyota’s NiMH Commitment

Toyota’s sustained commitment to NiMH in its hybrid lineup has been, arguably, the single most important factor in the technology’s commercial survival. Through its majority ownership stake in Primearth EV Energy Co. (PEVE) — a joint venture with Panasonic — Toyota maintained a vertically integrated NiMH supply chain that provided both cost control and supply security.

As of 2026, Toyota offers more than 20 hybrid vehicle models globally, most of which continue to use NiMH battery packs for the core hybrid battery system. This includes the Prius (now in its fifth generation), Corolla Hybrid, Camry Hybrid, RAV4 Hybrid, and multiple Lexus models. Honda similarly relies on NiMH in its e:HEV mild hybrid and full hybrid systems across the Civic, CR-V, and HR-V lines.

HEV Market Dynamics in 2026

The hybrid electric vehicle market has been one of the few bright spots in global automotive sales over the past three years, as consumers wary of pure battery-electric vehicles’ charging infrastructure limitations opted for hybrids as a practical middle ground. In Q1 2024, hybrid, battery electric, and plug-in hybrid vehicles collectively accounted for 22% of U.S. light-duty vehicle sales, up from 18% in Q1 2023 — a pace of adoption that has continued into 2026.

Crucially for NiMH, the growth segment has not been plug-in hybrids (which typically use lithium-ion for their larger battery packs) but conventional non-plug-in hybrids — precisely the application where NiMH’s cycle tolerance, thermal behavior, and cost profile make it the preferred choice. The Prius alone outsold every non-Tesla EV in the U.S. in January 2026, recording 3,093 hybrid units and 800 PHEV units in a single month.

The Replacement Battery Market Is Largely Invisible — and Substantial

Beyond new vehicle sales, the NiMH automotive market has a second revenue stream that most analyses undercount: replacement battery packs for the existing hybrid vehicle fleet. A Toyota Prius NiMH battery pack has a typical service life of 8–15 years depending on climate and use patterns. The global installed base of NiMH-powered hybrid vehicles now numbers in the tens of millions — a fleet that will generate billions of dollars in replacement pack demand over the next decade regardless of new vehicle sales trends.

This aftermarket demand is structurally insulated from the battery technology competition narrative. The 2012 Prius on your neighbor’s driveway cannot be upgraded to lithium-ion without a prohibitively expensive conversion. It needs a NiMH replacement pack, and the owner will buy one as long as the vehicle is worth keeping. That locked-in replacement cycle provides NiMH manufacturers with a revenue base that has almost no technology substitution risk.

Low Self-Discharge: The Quiet Product Revolution Nobody Talks About

One of the most consequential developments in the NiMH category over the past 15 years received almost no mainstream technology coverage: the commercialization of low self-discharge (LSD) NiMH chemistry, pioneered most successfully by Panasonic’s Eneloop brand.

Traditional NiMH batteries lose approximately 20–30% of their stored charge per month through self-discharge. This was a significant practical limitation — a battery charged in October and stored until December would be nearly dead by the time you needed it. For consumers accustomed to alkaline primary batteries (which self-discharge at roughly 2% per year), this behavior made standard NiMH cells frustrating to use.

What LSD NiMH Changed

LSD NiMH batteries, first introduced by Sanyo (later acquired by Panasonic and rebranded as Eneloop) in 2005, reduced the monthly self-discharge rate to approximately 1–2% per month — a reduction of roughly 90%. Eneloop cells can retain up to 70% of their charge after 10 years of storage, and up to 85% after 1 year. This fundamentally changed the usability profile of rechargeable NiMH batteries for consumer applications.

The commercial impact was significant. The ultra-low self-discharge NiMH segment — which includes Eneloop and competing products from brands like Varta, Duracell, and various private-label manufacturers — reached a market valuation of approximately $712 million in 2024, projected to grow to $1.06 billion by 2032 at a 6.3% CAGR. This segment is growing faster than the overall NiMH market, driven by consumer demand for sustainable, rechargeable alternatives to disposable alkaline batteries.

The Environmental Tailwind

The LSD NiMH segment is benefiting from a genuine, measurable consumer shift toward rechargeable batteries driven by environmental awareness. A single set of quality LSD NiMH AA cells can replace approximately 500–1,000 disposable alkaline batteries over its service life. As municipal battery recycling programs expand and environmental regulations on alkaline battery disposal tighten in markets including the EU and Canada, the case for LSD NiMH as the responsible consumer choice has become increasingly mainstream.

The EU’s updated Battery Regulation (2023/1542), which came into full force in 2026, sets binding targets for battery collection and recycling rates and imposes sustainability labeling requirements. NiMH’s established recycling infrastructure — built around its nickel content — positions it favorably compared to alkaline cells, which currently have low recycling rates in most markets.

The Supply Chain Story: Nickel, Rare Earths, and Geopolitical Tension

No honest analysis of the NiMH battery market in 2026 can ignore the raw material dynamics, because they represent both the market’s most significant risk factor and — paradoxically — one of its structural advantages over other battery chemistries.

NiMH batteries require nickel (the largest single material cost input), cobalt, rare earth elements (primarily lanthanum, cerium, and other lanthanides used in the metal hydride alloy), and manganese. The supply picture for each of these materials has shifted meaningfully in the past three years.

Indonesia’s Nickel Export Policies

Indonesia holds the world’s largest nickel reserves and in recent years has implemented increasingly strict export restrictions on raw nickel ore, requiring more ore processing to happen domestically before export. These policies, while intended to build Indonesia’s domestic battery and stainless steel industries, have created real cost pressure for NiMH manufacturers who previously sourced raw or partially refined nickel from Indonesian suppliers.

The effect on NiMH battery production costs has been meaningful but not catastrophic. Manufacturers with longer supply agreements and those using secondary (recycled) nickel have been more insulated. But the trend bears watching: if Indonesia’s export policies tighten further, or if similar restrictions emerge in the Philippines and New Caledonia (two other significant nickel producers), the cost advantage that NiMH holds over lithium-iron-phosphate (LFP) batteries in automotive applications could narrow.

The Russia-Ukraine Factor

Russia is one of the world’s top three producers of refined nickel, and the ongoing conflict in Ukraine — now entering its fourth year with no clear resolution in 2026 — continues to create volatility in global nickel markets. While Russian nickel has not been subject to comprehensive Western sanctions (unlike oil and gas), the logistical disruptions, banking restrictions, and reputational risks associated with Russian supply chains have pushed many European and North American manufacturers to reduce their exposure to Russian nickel, tightening supply and supporting price levels.

This matters for NiMH because nickel price volatility flows directly into battery manufacturing costs. A sustained increase in nickel prices disproportionately affects NiMH relative to lithium chemistries that use less nickel per unit of energy stored.

The Recycling Hedge

The mitigation strategy that sophisticated NiMH manufacturers are actively building is secondary material recovery. Spent NiMH batteries — particularly from hybrid vehicle packs — contain recoverable nickel, cobalt, and rare earth elements in concentrations that make recycling economically viable at scale. Companies like Umicore in Belgium and several Japanese recycling specialists have built industrial-scale NiMH recycling operations that can recover 95%+ of the nickel content from spent cells.

This creates a closed-loop supply chain dynamic that reduces raw material dependency. As the fleet of end-of-life hybrid vehicles grows — and tens of millions of first-generation Prius and Civic Hybrid units approach the end of their service lives — the volume of recyclable NiMH material entering the market will increase substantially, potentially offsetting some of the primary supply pressure from Indonesian and Russian geopolitics.

Asia-Pacific’s Iron Grip on NiMH Production

The NiMH battery market has a pronounced geographic concentration on the production side that shapes nearly every aspect of global supply, pricing, and competitive dynamics. Asia-Pacific dominates NiMH manufacturing, accounting for approximately 44.5% of global market share in 2026 — and within that region, Japan and China are the decisive forces.

Japan: Where Quality and Automotive Integration Meet

Japan’s NiMH industry is characterized by its deep integration with the automotive sector. Companies like Primearth EV Energy Co. (majority-owned by Toyota), Panasonic Energy, and FDK Corporation produce the high-specification NiMH packs used in Toyota and Honda hybrid vehicles. Japanese NiMH manufacturing operates at extremely high quality tolerances — automotive-grade cells must meet cycle life, capacity retention, and safety specifications that consumer-grade production does not require.

The Japanese market also leads in LSD NiMH technology. Panasonic’s Eneloop and Eneloop Pro lines are manufactured in Japan and command significant price premiums over Chinese-made alternatives, sustained by their documented superior performance in independent third-party testing. This premium positioning gives Japanese manufacturers a defensible market niche even as Chinese competitors have expanded aggressively into the commodity NiMH segment.

China: Scale, Cost, and Rapid Capacity Expansion

China’s NiMH production base is fundamentally different from Japan’s in both orientation and competitive strategy. Chinese manufacturers — led by companies including Highpower International, BYD’s legacy NiMH operations, and numerous smaller Guangdong-province producers — compete primarily on cost and scale. Chinese NiMH cells dominate the consumer electronics segment globally, powering everything from wireless keyboards and computer mice to children’s toys and garden lights.

China also controls a significant share of the rare earth element production that NiMH alloys require. China’s dominance in rare earth mining and processing — the country produces approximately 60–70% of global rare earth output — gives Chinese NiMH manufacturers a structural input cost advantage that is extremely difficult for non-Chinese producers to replicate. This advantage has enabled Chinese manufacturers to undercut Japanese and European competitors in commodity segments, though the quality gap remains meaningful in high-specification automotive and medical applications.

North America and Europe: Market Share Without Manufacturing Scale

The United States represents approximately 26% of global NiMH market revenue — roughly $800 million annually by 2026 estimates — but has minimal domestic manufacturing capacity. The U.S. NiMH market is predominantly served by imports from Japan and China, creating a supply chain dependency that has attracted limited but growing policy attention in the context of broader battery supply chain security initiatives.

Europe’s position is similar: a significant consumer of NiMH batteries (particularly for hybrid vehicles assembled in Europe by Toyota, Honda, and Ford) with limited indigenous production. The EU’s Battery Regulation and Critical Raw Materials Act have created some policy incentives for European NiMH production investment, but meaningful manufacturing scale in Europe remains a medium-term prospect at best.

The Six Applications Keeping NiMH Alive Beyond Cars

While hybrid vehicles dominate the NiMH revenue picture, the market’s resilience also depends on a diversified base of secondary applications. These applications rarely generate headlines, but they collectively represent more than half of NiMH market volume and provide important demand diversification that insulates the market against any single-application slowdown.

1. Consumer Electronics

Consumer electronics remain a meaningful NiMH segment, particularly in the AA and AAA form factors used by wireless peripherals, remote controls, toys, portable audio devices, and photography equipment. The global AA battery market alone is valued at over $8 billion in 2026, with NiMH rechargeable cells holding a growing share of that market. The transition from disposable alkaline to rechargeable NiMH is slow but measurable, driven by cost economics over time and growing environmental awareness.

2. Medical Devices

Medical applications represent one of the highest-value NiMH segments. Portable diagnostic equipment, infusion pumps, pulse oximeters, blood pressure monitors, and emergency defibrillators frequently use NiMH batteries because of their predictable discharge characteristics, lack of memory effect in modern formulations, and established regulatory compliance history. Medical device manufacturers value the extensive safety and performance data that exists for NiMH chemistry across decades of real-world use — data that newer chemistries cannot yet match.

3. Power Tools

The cordless power tool segment was one of NiMH’s early growth drivers and remains a meaningful application area, though lithium-ion has taken significant market share at the premium end. NiMH continues to hold ground in entry-to-mid-market cordless tools where the cost premium of lithium-ion cannot be justified and the weight-to-performance ratio of NiMH is acceptable. This segment has shrunk as a percentage of overall NiMH volume but remains commercially significant in developing markets where price sensitivity is higher.

4. Emergency Lighting and Backup Power

Emergency lighting systems, UPS (uninterruptible power supply) units, and backup power applications use NiMH for its long standby life, reliable discharge characteristics, and wide operating temperature range. In commercial and industrial buildings, NiMH emergency lighting packs must comply with safety standards that have historically favored chemistries with well-established failure mode behavior — again advantaging NiMH’s decades-long track record over newer alternatives.

5. Cordless Telephones and Communication Devices

The cordless telephone market has declined significantly with smartphone adoption, but NiMH remains the dominant battery chemistry in the cordless phone units still in use globally — a market larger than most North American observers appreciate, particularly in developing markets where landline infrastructure remains important. This segment is in structural decline but still generates meaningful NiMH revenue in the near term.

6. Industrial Automation and Robotics

One of the most interesting emerging NiMH applications is in industrial automation — specifically in automated guided vehicles (AGVs), warehouse robots, and light industrial equipment where the duty cycle involves repeated short-distance travel, frequent regenerative braking-style energy recovery, and operation in environments where lithium-ion’s thermal management requirements create engineering complications. The parallels to hybrid vehicle use cases are not coincidental: the same NiMH properties that work well in a Prius work well in a warehouse robot that travels the same route hundreds of times per day.

Who’s Winning in the NiMH Market Right Now

The NiMH competitive landscape in 2026 is more concentrated than many market participants realize. A handful of large, vertically integrated manufacturers control the majority of global capacity and supply, particularly in the high-value automotive segment.

Primearth EV Energy Co. (PEVE)

PEVE, the Toyota-Panasonic joint venture, is the world’s largest producer of automotive-grade NiMH battery packs by volume. Operating exclusively in Japan, PEVE supplies the NiMH packs for Toyota’s and Lexus’s hybrid models globally. Its deep integration into Toyota’s just-in-time manufacturing supply chain gives it structural advantages that no competitor has been able to replicate — and Toyota’s ongoing commitment to NiMH in its non-plug-in hybrid lineup ensures PEVE’s demand base through at least the early 2030s.

Panasonic Energy (Consumer Division)

Panasonic’s consumer battery division, which produces the Eneloop LSD NiMH line alongside conventional NiMH cells, is the market leader in the premium consumer rechargeable segment. Eneloop commands retail prices 30–50% above commodity NiMH competitors, sustained by third-party performance verification and strong brand loyalty among photography and audio enthusiasts, emergency preparedness communities, and sustainability-conscious consumers. The Eneloop Pro variant (2550mAh AA, 500-cycle rated) represents the current benchmark that competitors measure against.

FDK Corporation

FDK, a subsidiary of Fujitsu and Furukawa Electric, is a major NiMH manufacturer supplying both consumer and industrial markets from its Japanese facilities. FDK manufactures the NiMH cells used in many medical devices and also produces the batteries under white-label arrangements for several major retail brands globally.

Highpower International

Listed on the New York Stock Exchange (HPJ), Highpower International is China’s largest NiMH exporter and one of the few Chinese battery companies with significant sales into North American and European consumer markets. Highpower’s strategy of combining NiMH production with lithium-ion capacity gives it flexibility to serve customers across battery chemistry categories — a strategic hedge that pure-play NiMH manufacturers do not have.

The Lithium-Ion Comparison: Why It’s More Complicated Than You Think

The NiMH-versus-lithium-ion debate is often presented as a simple technology adoption story: newer, better chemistry displaces older, inferior one. The reality on the ground in 2026 is considerably more nuanced, and the nuances have material commercial implications.

The LFP Factor

One of the most important recent developments in the battery competitive landscape is the rapid cost reduction and market penetration of lithium-iron-phosphate (LFP) batteries. LFP cells — used extensively by BYD, CATL, and Tesla (in its standard range vehicles) — have closed much of the cost gap with NiMH while offering higher energy density and faster charging. LFP represents a more credible threat to NiMH’s automotive dominance than nickel-rich NCM or NCA lithium-ion chemistries, because LFP’s safety profile and thermal stability are closer to NiMH’s.

However, LFP batteries still require sophisticated battery management systems (BMS) for automotive applications, carry higher upfront manufacturing cost relative to NiMH at comparable scales, and are more sensitive to low-temperature performance degradation than NiMH — a non-trivial issue in markets like Canada, Northern Europe, and Northeast Asia where winter temperatures regularly affect battery performance.

The BEV Versus HEV Distinction Is Critical

A common analytical error is treating all electrified vehicles as interchangeable when comparing battery chemistry competition. Battery electric vehicles (BEVs) overwhelmingly use lithium-ion, and NiMH is not a meaningful competitor in that application — the energy density gap is too large for the 60–100+ kWh packs that BEVs require. But conventional non-plug-in hybrids use battery packs in the 1.2–2.0 kWh range, where NiMH’s cost, cycle tolerance, and thermal behavior advantages over lithium-ion are meaningful.

The competitive question for NiMH is therefore not “will it replace lithium-ion in BEVs?” (it won’t) but “will lithium-ion replace NiMH in conventional hybrids?” The answer, at least through 2030, appears to be: partially, slowly, and not completely. Several major automakers are selectively transitioning some hybrid models to lithium-ion for reasons of energy density and cost trajectory, but Toyota — which accounts for a disproportionate share of global NiMH hybrid demand — has explicitly stated its intention to maintain NiMH in its core hybrid lineup for the foreseeable future based on total cost of ownership and reliability data from its global fleet.

Total Cost of Ownership Tells a Different Story Than Sticker Price

When evaluating NiMH versus lithium-ion in the applications where they actually compete, total cost of ownership (TCO) analysis frequently surprises observers who assume newer must mean cheaper. For a mid-volume consumer electronics manufacturer sourcing AA-format rechargeable cells, the TCO of NiMH — accounting for mature supply chain pricing, established testing infrastructure, regulatory compliance history, and recycling costs — is often lower than an equivalent lithium-ion solution, which requires additional circuit protection, specialized chargers, and more complex handling and shipping compliance.

This TCO reality is one reason NiMH maintains positions in industrial, medical, and consumer applications where a simple chemistry substitution would seem straightforward but proves economically unattractive on closer examination.

What the Next Seven Years Look Like for NiMH

Looking at the period from 2026 to 2033, the NiMH market trajectory is one of moderate but durable expansion, shaped by several converging forces that will determine whether the upper or lower end of current forecasts — $4.1 billion to $4.9 billion — proves accurate.

The HEV Sales Trajectory Will Be the Master Variable

Everything in the NiMH forecast flows from hybrid vehicle sales. If global HEV sales continue to grow at their recent pace — driven by consumer preference for the extended range and infrastructure independence that non-plug-in hybrids offer — NiMH demand will remain robust through the early 2030s even if the automotive industry is also building more BEVs and PHEVs in parallel.

The key risk scenario for NiMH is an accelerated transition away from conventional hybrids toward plug-in hybrids or BEVs — a shift that could occur if charging infrastructure improves rapidly, if battery costs for large packs fall faster than expected, or if government incentive structures more heavily penalize non-plug-in hybrids. Under that scenario, NiMH demand could plateau earlier than current forecasts suggest.

High-Capacity NiMH Assemblies: The Fast-Growing Niche

Within the broader NiMH market, the high-capacity assembly segment — larger NiMH packs used in telecom backup power, stationary storage in high-temperature climates, and off-grid energy systems — is growing at approximately 6.8% CAGR, faster than the overall market. In developing markets across Southeast Asia, Africa, and parts of South America, NiMH’s thermal resilience in hot climates and its lower technology support burden (compared to lithium-ion BMS requirements) make it the practical choice for backup power applications where service infrastructure is limited.

Technology Developments to Watch

NiMH is not a static technology. Active research and development continues on several fronts:

- High-capacity electrode development: Researchers are working on enhanced metal hydride alloy compositions that can increase NiMH energy density toward the 150 Wh/kg range, which would meaningfully close the gap with LFP lithium-ion while retaining NiMH’s thermal and safety advantages.

- Nano-structured alloys: Nanostructured anode materials are showing improved hydrogen storage capacity and faster charge kinetics in laboratory settings, with some results suggesting cycle life improvements of 20–30% over conventional NiMH alloys.

- Recycling technology scaling: Improved hydrometallurgical processes for recovering rare earth elements from spent NiMH cells are being commercialized in Europe and Japan, which could meaningfully reduce raw material costs for manufacturers with access to end-of-life vehicle battery streams.

The Regulatory Environment Favors Durability

The EU Battery Regulation, North American critical minerals policies, and emerging Asian recycling mandates all create regulatory environments that reward batteries with established recycling infrastructure and well-characterized environmental profiles. NiMH, as a technology with 30+ years of safety data and functioning recycling systems, is advantaged in this regulatory context relative to newer chemistries that are still building their compliance and recycling infrastructure.

Takeaways for Investors, Engineers, and Business Leaders

The NiMH growth story is not a simple “buy the rocket ship” narrative. It is a more disciplined story about market durability, application specificity, and the compounding value of getting a technology right for a specific use case and then defending that position with relentless cost and quality discipline. Here is what the data actually suggests for different audiences:

For Investors and Market Analysts

The NiMH market is not a high-growth opportunity in the conventional venture or growth equity sense. A 3–4.5% CAGR does not produce the kind of returns that attract growth capital. What it does offer is significant stability and predictable demand driven by a large, locked-in automotive replacement market that has limited technology substitution risk through the early 2030s. For investors in publicly traded NiMH-exposed companies — including Highpower International, Panasonic Holdings, and companies with NiMH materials supply exposure like nickel miners — understanding the automotive replacement cycle dynamics is more important than tracking new vehicle sales headlines.

The secondary nickel and rare earth recovery opportunity is the higher-growth adjacent play. Companies building industrial-scale NiMH recycling capacity are positioned to benefit from both the volume growth in end-of-life hybrid batteries and the regulatory tailwinds supporting secondary material recovery. This is a less obvious but potentially more attractive investment angle than the battery manufacturers themselves.

For Engineers and Product Teams

The persistent choice between NiMH and lithium-ion should always be run as a genuine TCO analysis rather than a default “use the newer chemistry” decision. For applications with duty cycles similar to hybrid vehicle regenerative braking — frequent shallow cycling, temperature extremes, long calendar life requirements, and constrained thermal management budgets — NiMH continues to offer engineering advantages that are frequently underweighted in early-stage product decisions driven by energy density specifications alone.

Specifically: if your application requires operation below -20°C or above 45°C without active thermal management, if your expected cycle count is above 100,000 shallow cycles, or if your regulatory environment rewards established safety data records over projected performance, NiMH warrants serious evaluation even in 2026.

For Supply Chain and Procurement Leaders

The geopolitical risk profile of NiMH raw materials — particularly nickel exposure to Indonesian export policy and rare earth exposure to Chinese processing dominance — warrants active monitoring and hedging. Organizations with significant NiMH procurement volumes should be exploring supply agreements with secondary material processors, qualifying multiple geographic sources for key alloy components, and modeling the cost impact of nickel price scenarios given current Indonesian and Russian supply dynamics.

The good news: the NiMH recycling infrastructure is mature enough that secondary-source raw material contracts are commercially available and economically viable for medium-to-large procurement volumes. This is a risk mitigation lever that remains underutilized by many procurement organizations.

For Business Leaders Thinking About the Broader Energy Transition

The NiMH story contains a broader lesson about technology transitions that applies well beyond the battery industry. The conventional narrative of technology adoption — new chemistry arrives, old chemistry fades — consistently underestimates how long incumbents with specific performance advantages in specific applications can sustain commercial relevance. NiMH was “going to be replaced” by lithium-ion in hybrid vehicles in the late 1990s, then again in the mid-2000s, and the conversation is still ongoing in 2026.

The reason is not inertia or ignorance. It is that real-world application requirements are more complex than laboratory specifications suggest, switching costs in validated applications are higher than they appear, and the total cost calculus — including supply chain stability, regulatory compliance, and service infrastructure — frequently favors the known over the theoretically superior.

Understanding this dynamic in your own industry — wherever you sit in the energy, materials, or manufacturing sectors — may be the most durable insight this 25,200% growth story actually offers.

The Verdict: A Market Worth Understanding on Its Own Terms

The nickel-metal hydride battery market in 2026 is worth approximately $3.5 billion, growing toward $4.9 billion by 2033, anchored by hybrid vehicle demand that accounts for nearly half its revenue, diversified across six meaningful secondary applications, concentrated in Asia-Pacific production but global in consumption, and facing specific supply chain risks that are manageable but not trivial.

The 25,200% cumulative growth figure is not a marketing invention. It is an accurate representation of the distance this technology has traveled from commercial inception to present maturity — and it tells a story about durability, specific-application excellence, and the long-term value of cost and quality discipline that pure growth metrics cannot capture.

NiMH will not headline the next wave of battery technology coverage. Solid-state, sodium-ion, and next-generation lithium chemistries will dominate that conversation. But the factories in Japan and China producing NiMH cells today will be running in 2033, and the hybrid vehicles on the roads of North America, Europe, and Asia will still be running on NiMH packs. In a sector defined by hype cycles and premature obituaries, that kind of sustained, unglamorous commercial relevance deserves its own accounting.

And by that accounting, the NiMH battery market has done something genuinely notable: it turned a 1990s laboratory chemistry into a multi-billion-dollar global industry and held its ground long enough to matter again in the age of electrification.